India: The World's First Electrostate

How 1.4 billion people are about to skip the fossil fuel era entirely

Every country that has industrialized has followed the same playbook: burn coal, pump oil, get rich, then clean up the mess.

Britain did it. America did it. China perfected it.

India is about to tear up that playbook.

What India is doing right now — quietly, methodically, at astonishing scale — has no historical precedent. It is attempting to become the first major economy in human history to reach prosperity without going through a fossil fuel phase. The first Electrostate.

And the data says it might actually pull it off.

The Playbook Everyone Else Followed

Let’s start with what “normal” looks like.

When countries develop, they follow a predictable energy curve. They burn biomass (wood, dung). Then they discover fossil fuels. Coal powers factories. Oil powers cars. GDP goes up. Carbon goes up. Eventually, when the country is rich enough to care about the environment, it starts building renewables to replace the fossil infrastructure it already built.

This is the path Britain took over 200 years. America took over 150. China compressed it into about 40.

The assumption embedded in every development economics textbook is that this sequence is inevitable. You must pass through the fossil fuel phase. It is the necessary price of admission to modernity.

India’s clean energy transition is proving that assumption wrong.

The Electrotech Shortcut

Think about what happened with telephones.

In the 1990s, the conventional wisdom was that developing countries needed to build landline networks before they could dream of widespread communication. Laying copper wire to every village, every house — that’s how the West did it.

Then mobile phones got cheap. And countries like India, Kenya, and China didn’t build landlines at all. They leapfrogged straight to mobile. India went from 5 million phone connections in 2001 to over 1.2 billion today — almost entirely wireless.

The same thing is happening with energy.

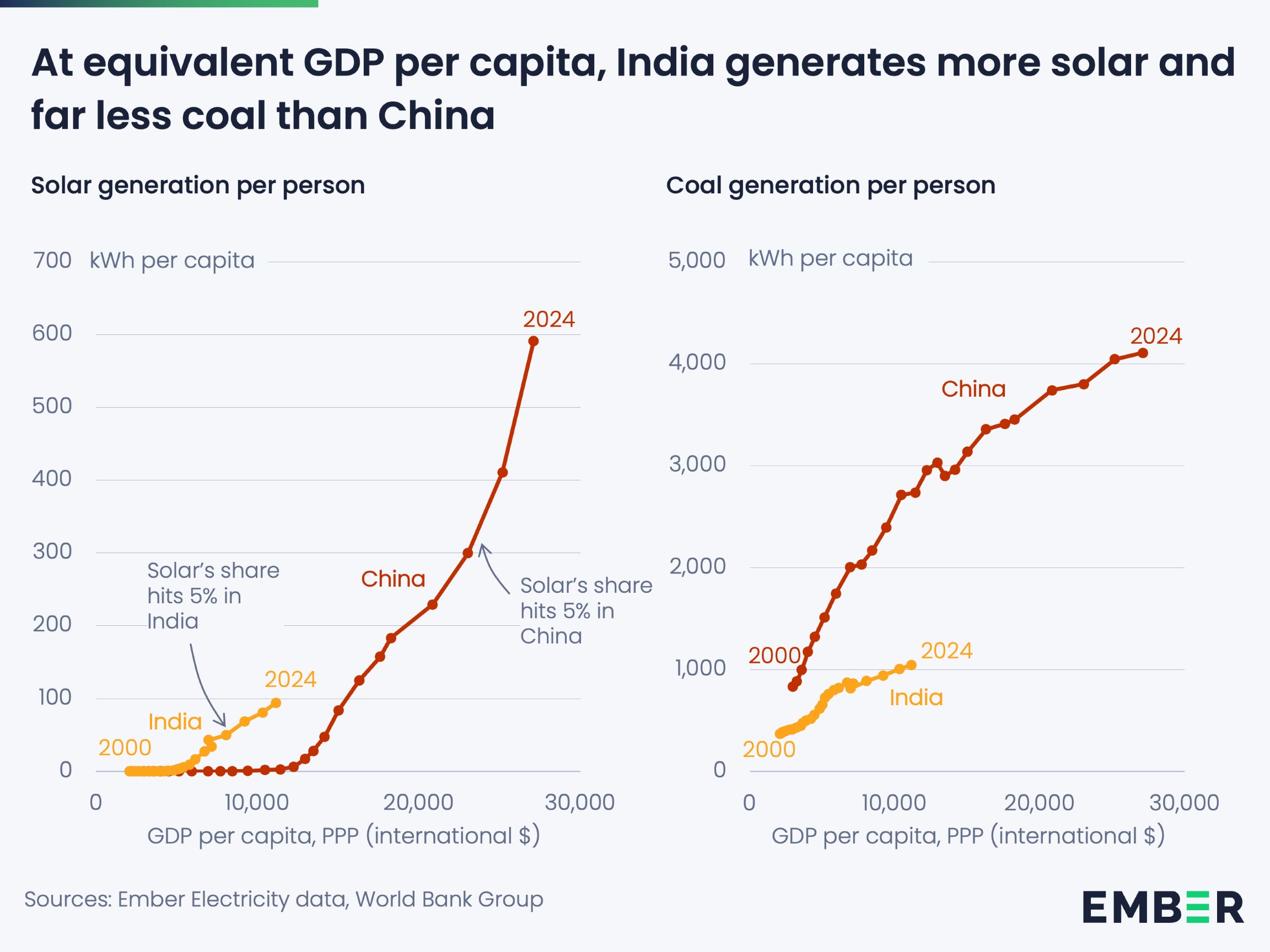

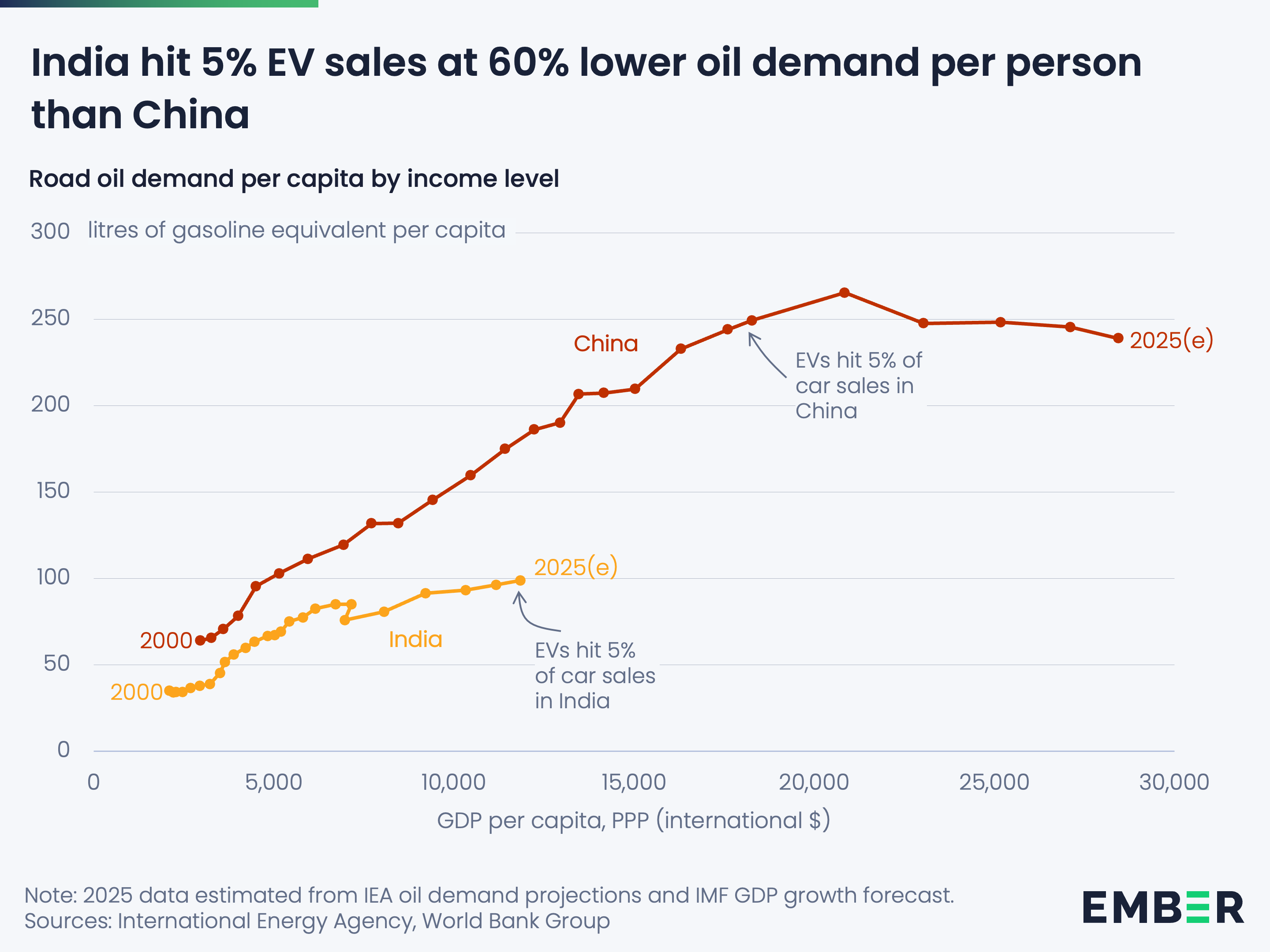

When China was at India’s current level of economic development (roughly $11,000 GDP per capita, PPP), solar power was a novelty. It was 2012. Solar accounted for essentially 0% of China’s electricity. The only option for powering factories was coal.

In 2025, solar accounts for 9% of India’s electricity. And the cost has collapsed so far that solar-plus-storage is now roughly half the cost of building new coal plants.

India isn’t building out a fossil fuel infrastructure and then planning to replace it. It is building the clean energy infrastructure first. This is the electrotech shortcut: skipping the fossil fuel detour entirely.

India’s Clean Energy Numbers Are Staggering

Let me walk you through what India has actually done.

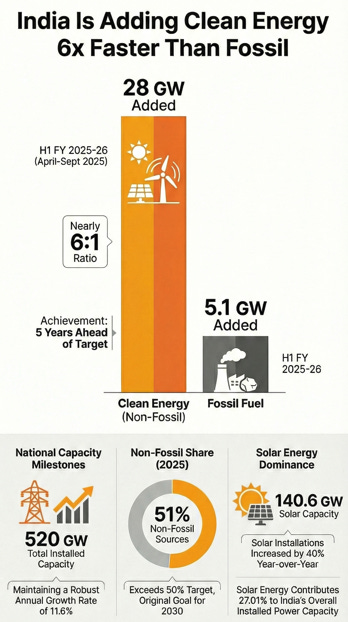

As of January 2026, India’s total installed power capacity crossed 520 GW — growing at an annual rate of 11.6%. To put that in perspective, India added more power capacity in a single year than most countries have in total.

Here’s the composition that matters:

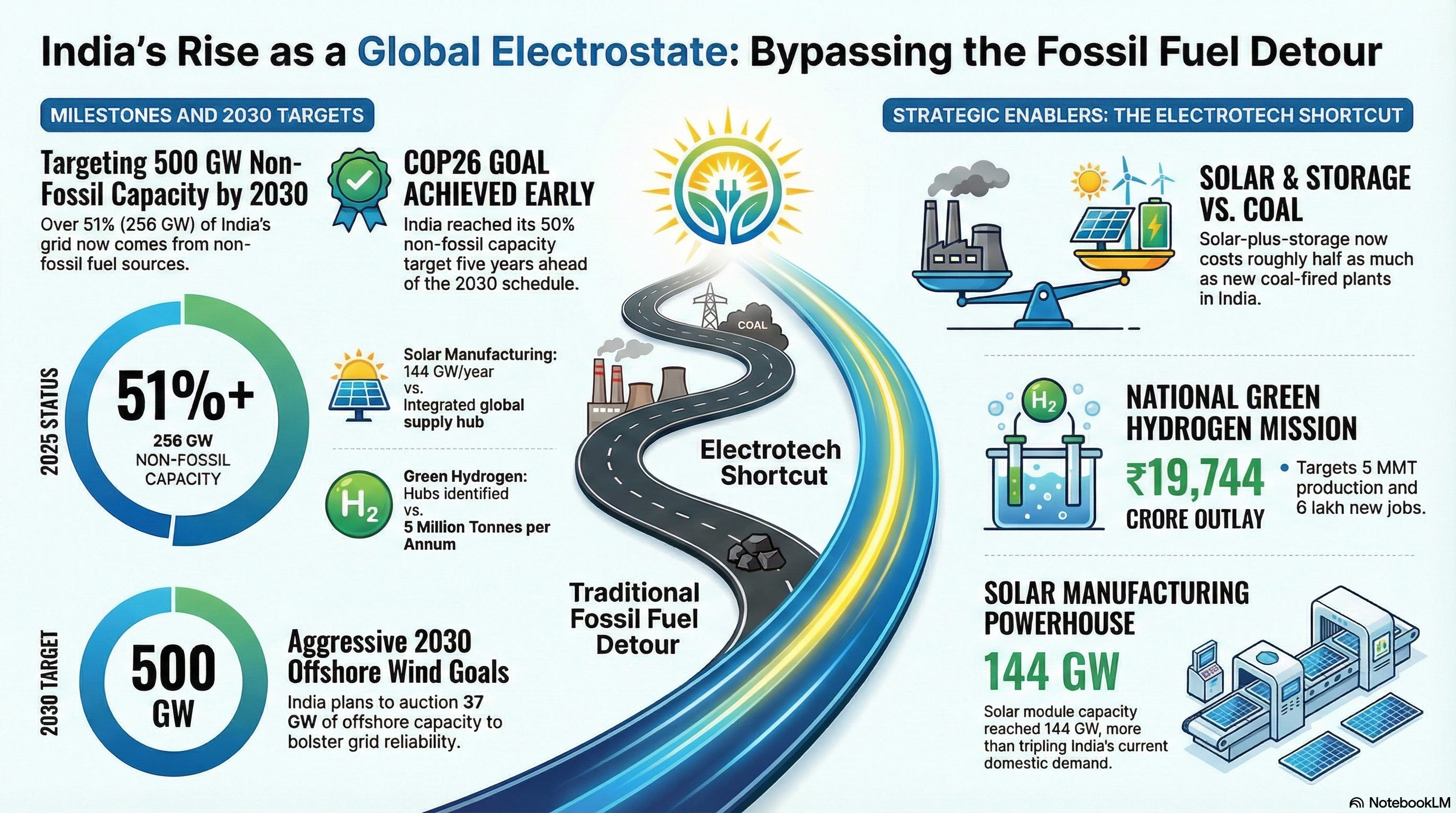

Non-fossil sources now account for over 51% of installed capacity. India hit this milestone in September 2025 — five years ahead of its 2030 target.

Solar alone reached 140.6 GW — up 40% from the previous year. Solar now represents 27% of India’s entire power capacity.

In the first half of FY 2025-26 alone, India added 28 GW of non-fossil capacity versus just 5.1 GW of fossil capacity. The ratio is nearly 6:1.

But the most telling comparison isn’t India against itself. It’s India vs China at the same stage of development.

India’s per capita coal generation is only 40% of what China’s was at equivalent GDP levels. India’s per capita road oil demand (96 liters to China’s 150) is roughly half of China’s at the same development stage.

India is reaching similar levels of electrification — about 20% of final energy — but doing it with roughly one-sixth the coal input.

Read that again. One-sixth!

Why India’s Energy Transition Is Happening Now

Three forces are converging to make this possible. Remove any one of them, and the electrostate thesis falls apart. Together, they make it nearly inevitable.

1. Timing: The Cost Collapse

India is industrializing at the exact moment in history when clean energy became cheap. This is the single most important fact.

When China industrialized in the 2000s, solar panels cost over $4 per watt. Today, they cost under $0.20. Battery storage costs have fallen by more than 90% in a decade.

The result: standalone battery storage tariffs in India dropped 75% between 2022 and early 2025 — from INR 11.25 lakh/MW to INR 2.19-2.40 lakh/MW. Solar-plus-battery tariffs fell from INR 6.99/kWh in 2018 to INR 3.32/kWh in 2025.

This isn’t a policy choice. It’s an economic reality. Renewable energy is now the cheapest option. India isn’t choosing virtue over growth. It’s choosing the cheapest electricity available.

2. Necessity: The Sovereignty Imperative

Unlike America, Russia, or Saudi Arabia, India has no significant domestic fossil fuel reserves. It imports roughly 5% of its GDP worth of oil and gas every year. This is an enormous strategic vulnerability.

Every barrel of imported oil is a transfer of wealth and leverage to other nations. Every gas pipeline is a geopolitical leash.

The electrostate path isn’t just cheaper — it’s a sovereignty play. A country that generates its own electricity from sunlight falling on its own land doesn’t need to worry about OPEC production cuts, Strait of Hormuz blockades, or Russian pipeline politics.

India has a term for this: energy self-reliance (atmanirbhar). And unlike most slogans, the economics actually back it up. India’s energy independence depends not on discovering new fossil reserves, but on harnessing the solar radiation that already falls on its territory — for free.

3. Structure: The Services Economy Advantage

India’s economy is fundamentally different from China’s. China’s growth was driven by heavy industry — steel mills, cement plants, construction. These are enormously energy-intensive.

India’s growth is driven by services — IT, finance, healthcare, education. India generates one-third more economic output per unit of energy than China.

This structural difference means India can reach high-income status with dramatically less energy consumption per capita. It doesn’t need to power blast furnaces. It needs to power data centers, air conditioners, and electric scooters.

And electricity is spectacularly good at powering all three.

The Solar Manufacturing Bet

“But wait,” the skeptics say. “India can’t be an electrostate if it’s importing all the components from China.”

Fair point. And India has an answer.

India’s solar PV module manufacturing capacity has exploded to 162 GW as of January 2026 — enough to be self-sufficient and then some. Cell manufacturing capacity reached 26 GW. Since 2022, module capacity increased by 216% and cell capacity by 344%.

The Production Linked Incentive (PLI) scheme for solar — with a total outlay of INR 24,000 crore — has attracted INR 52,900 crore in investment by September 2025 and created over 44,000 jobs. India is on track to become the world’s second-largest solar PV manufacturer after China.

Is it perfect? No. India still depends on China for upstream materials like polysilicon and wafers. The PLI execution has been uneven — only 31 GW of the targeted 65 GW module capacity has been commissioned. But the trajectory is unmistakable.

And it’s not just solar. India’s electronics industry has grown nearly sixfold — from $22 billion in FY2015 to about $130 billion in FY2025. The country is building the industrial base to manufacture the tools of the electrostate era.

Three Pillars of India’s Electrostate Future

An electrostate doesn’t just generate clean power. It needs to store it, move it, and use it to make things. India is building all three pillars simultaneously.

Pillar 1: Battery Storage and Pumped Hydro — The Backbone

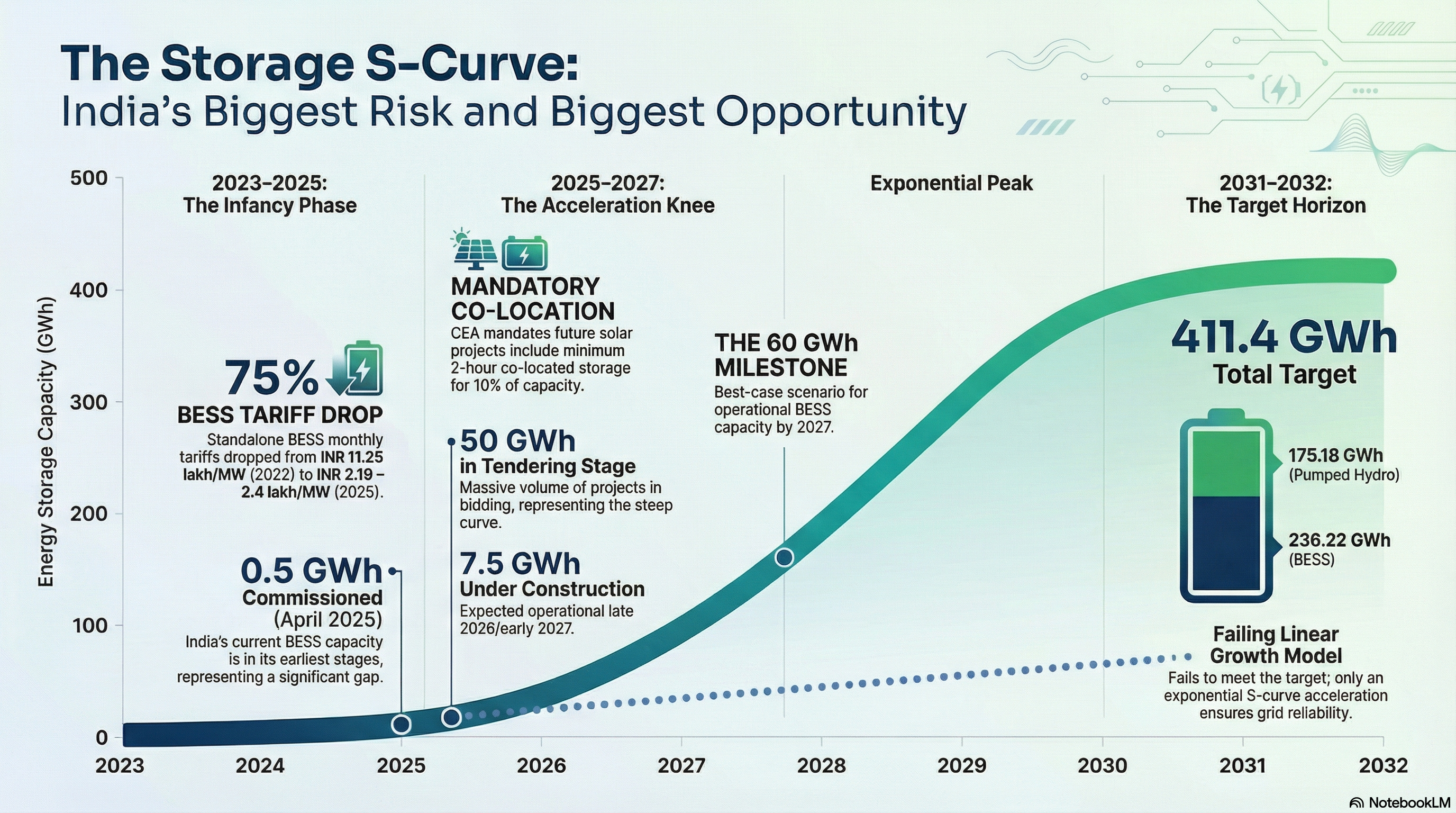

Solar power has an obvious limitation: the sun doesn’t shine at night. The electrostate needs massive energy storage.

India’s National Electricity Plan projects a requirement of 411.4 GWh of energy storage by 2031-32 — split between 236 GWh of batteries and 175 GWh of pumped hydro.

The current gap is enormous. As of April 2025, only about 0.5 GWh of battery storage capacity was operational in India. But the pipeline tells a different story: 7.5 GWh under construction, 50 GWh in tendering, and a government mandate that new solar projects include co-located storage (potentially adding 14 GW / 28 GWh by 2030).

Pumped hydro is moving too — 122 GWh announced, 39 GWh under execution. Andhra Pradesh alone is targeting 22 GW.

The gap between where India is and where it needs to be is the single biggest risk to the electrostate thesis. But costs are plummeting so fast that deployment tends to follow an S-curve — slow at first, then explosive.

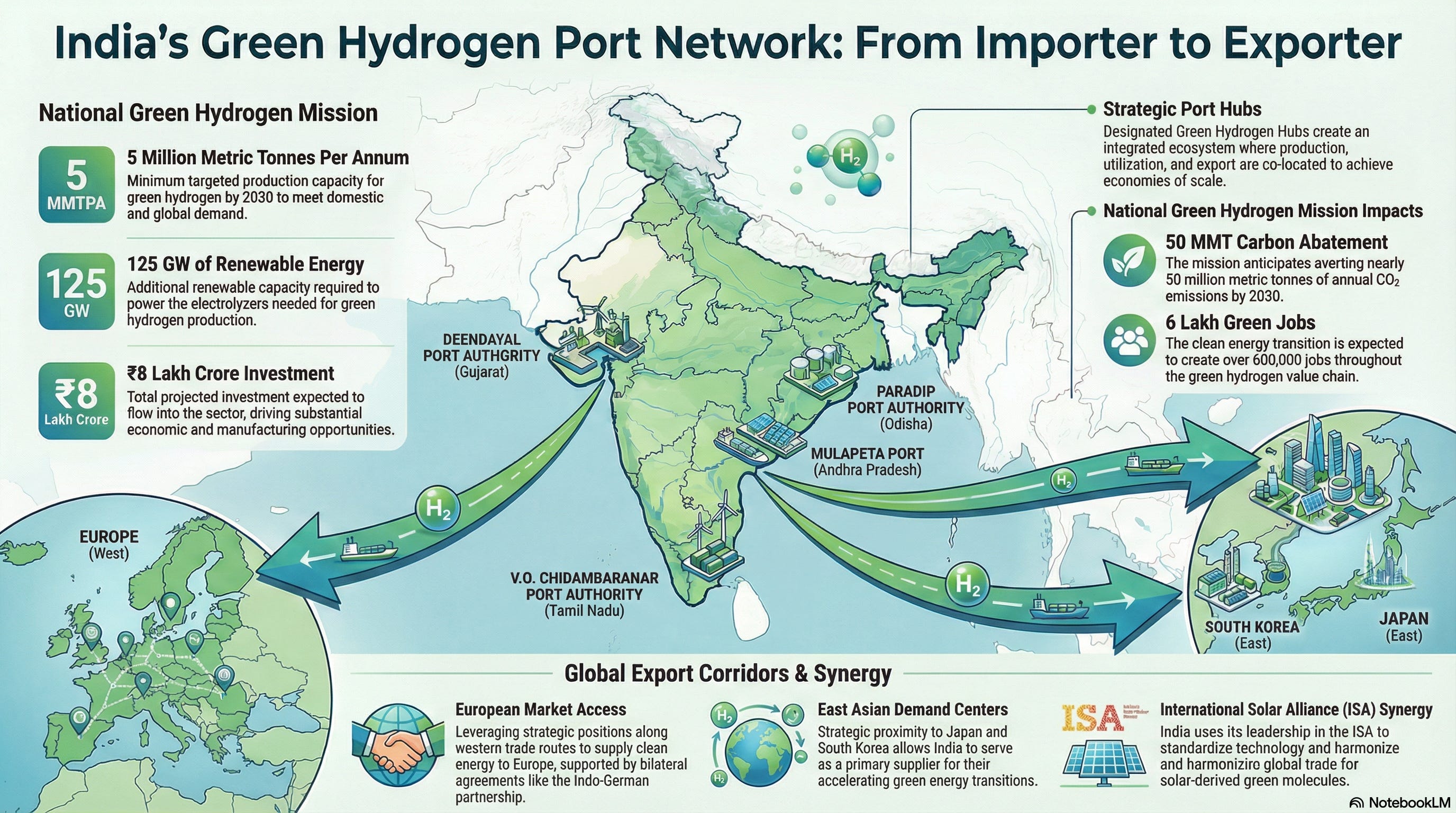

Pillar 2: Green Hydrogen — The Industrial Molecule

Some things can’t run on batteries. Steel. Cement. Shipping. Fertilizer. For these, India is betting on green hydrogen — hydrogen produced using renewable electricity.

The National Green Hydrogen Mission is among the most ambitious on the planet:

5 million metric tonnes per annum by 2030

Supported by 125 GW of additional renewable energy capacity

Total mission outlay of INR 19,744 crore, with expected investment exceeding INR 8 lakh crore

Three major ports — Deendayal (Gujarat), V.O. Chidambaranar (Tamil Nadu), and Paradip (Odisha) — designated as Green Hydrogen Hubs

A $1.3 billion project at Mulapeta port in Andhra Pradesh to create a global export hub for green hydrogen and ammonia by 2029

Electrolyser manufacturing contracts have been awarded for 3,000 MW of annual capacity. Green hydrogen production contracts cover 8.62 lakh tonnes per annum.

The ambition is not just to use green hydrogen domestically, but to become a global exporter — turning India’s abundant sunshine into a tradeable industrial commodity.

Pillar 3: Offshore Wind — The Missing Gigawatts

India’s solar story is well-known. Its offshore wind energy potential is the hidden giant.

India has set a target of 30 GW of offshore wind by 2030, with an auction trajectory of 37 GW. Tenders for 4 GW and 7 GW have been floated off the Tamil Nadu coast. Resource assessments show average wind speeds of 7.61 m/s off Gujarat, with capacity factors of 38% — significantly better than onshore wind’s 33%.

Offshore wind is crucial because it produces power at different times than solar, improving grid reliability. It’s the complement that makes the electrostate viable around the clock.

The Age of Electricity: Why Energy Demand Is Exploding

Here’s the bigger picture that makes all of this make sense.

We are entering what The Daily Brief by Zerodha called Age of Electricity — a structural shift where electricity demand decouples from GDP growth and accelerates far beyond it. India’s electricity demand is projected to grow 3.6% annually through 2030, outpacing economic growth.

The drivers are everything that defines modern life:

Air conditioning. Temperature sensitivity of electricity demand in states like Uttar Pradesh has increased fivefold. As India gets richer, hundreds of millions of people will buy their first AC unit.

Data centers and AI. Computation is the new heavy industry, and it runs on electricity.

Electric transport. India is already the global leader in electric three-wheeler sales. EVs accounted for roughly 5% of car sales by mid-2025.

This isn’t just India’s story. Globally, carbon emissions from the power sector are plateauing even as electricity demand skyrockets. The historic link between growth and pollution is breaking.

But India is the country best positioned to ride this wave, because it’s building the infrastructure for the Age of Electricity from scratch rather than retrofitting a legacy fossil system.

The Risks Are Real

I’d be lying if I said this was a sure thing. The electrostate thesis has genuine vulnerabilities.

The grid bottleneck is severe. Renewables take 1-5 years to build. Transmission infrastructure takes 5-15 years. This mismatch means India could have the generation capacity but not the wires to deliver it. Globally, over 2,500 GW of projects are waiting for grid connections.

The storage gap is enormous. 0.5 GWh deployed against a 411 GWh target is a 800x gap. Even with aggressive deployment, hitting that target by 2032 requires exponential scaling.

Coal isn’t going away tomorrow. At 42.5% of installed capacity, coal remains India’s largest single power source. India is still considering plans to expand coal output. The transition is not a light switch — it’s a long ramp.

Supply chain dependency on China for upstream materials (polysilicon, battery cells) is a strategic risk that mirrors the very fossil fuel import dependency the electrostate model is supposed to solve.

Grid stability under high renewable penetration is an unsolved engineering challenge. The Spain-Portugal grid collapse of 2025 was a warning of what happens when variable renewables overwhelm grid management systems.

What India’s Electrostate Means for the World

If India succeeds — even partially — in becoming an electrostate, it rewrites the rules of development economics for every country that follows.

For developing nations: India is the proof of concept. If a country of 1.4 billion people with a per capita income of $2,800 can industrialize on clean electricity, then the “you need fossil fuels first” argument is dead. Every country in Africa, Southeast Asia, and Latin America will have a template.

For the climate: India reaching $20,000 GDP per capita without passing through China’s coal peak would be the single largest positive climate event in human history. It would mean 1.4 billion people reaching middle-income status while generating a fraction of the carbon.

For geopolitics: An India that generates its own power from its own sunlight is an India that doesn’t need Middle Eastern oil, Russian gas, or Australian coal. Energy sovereignty reshapes alliances, trade balances, and diplomatic leverage.

For investors: The electrostate is a $8+ lakh crore investment opportunity in green hydrogen alone. Add solar manufacturing, battery storage, offshore wind, grid infrastructure, and EVs, and you’re looking at one of the largest capital deployment opportunities of the 21st century.

The Bottom Line

Every major economy in history has been built on fossil fuels. Every single one.

India is attempting something that has never been done: building a $10 trillion economy powered primarily by electrons harvested from sunlight, wind, and flowing water. An economy where energy is not imported but generated. Where the fuel is free and the infrastructure is the asset.

The data says India is further along this path than most people realize. 520 GW of capacity. 51% non-fossil. 140 GW of solar. Manufacturing scaling at triple-digit growth rates. Green hydrogen ports under construction. Storage costs in freefall.

Is it guaranteed? No. The grid, the storage gap, and the China supply chain are real risks.

But the direction is unmistakable. The cost curves are unforgiving. And the momentum is accelerating.

India isn’t just adding renewables to its grid. It is building a new model of civilization — one where prosperity and pollution are finally, permanently decoupled.

The world’s first electrostate is being built in real time.

And most people haven’t noticed yet.

Also, if you liked this deep dive, you may also enjoy one of my favorite explorations yet, on the ever-fascinating ISRO:

India Was the Poorest Nation to Launch a Space Program. Here's How ISRO Outpaced Europe.

How India Launched a Space Program at $107 Per Capita GDP

Sources & Further Reading

“India’s Electrotech Shortcut: Bypassing the Fossil Fuel Detour” — Ember/Niti Aayog Analysis

“India Poised To Become World’s First Electrostate?” — CleanTechnica

“India Crosses 520 GW Power Capacity As Solar Reaches 140.6 GW In January 2026” — Mercom India

“India hits 500 GW in installed power, over 50% from non-fossil sources” — Enerdata

“India’s Journey to 500 GW Non-Fossil Fuel Capacity: Storage as the Backbone” — JMK Research

“Assessing the Value of Offshore Wind for India’s Power System in 2030” — CEEW

“National Green Hydrogen Mission” — Press Information Bureau, Government of India

“Three Major Ports Recognised as Green Hydrogen Hubs” — PIB Press Release

“Assessing the effectiveness of India’s solar Production Linked Incentive scheme” — JMK Research & Analytics

“EDF India releases white paper on pumped storage investment framework”

“Renewable Energy: How international collaboration is accelerating India’s solar and green hydrogen push”

“The age of electricity” — The Daily Brief by Zerodha